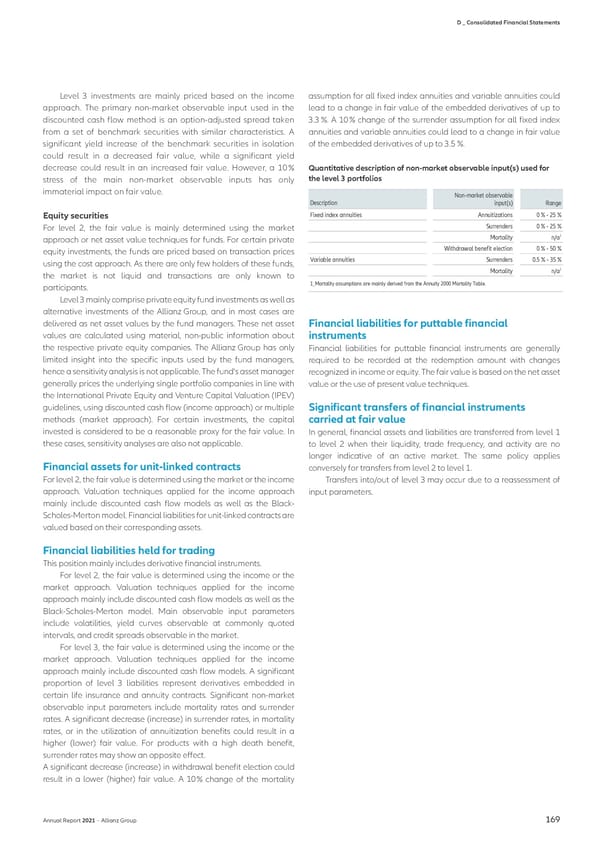

D _ Consolidated Financial Statements Level 3 investments are mainly priced based on the income assumption for all fixed index annuities and variable annuities could approach. The primary non-market observable input used in the lead to a change in fair value of the embedded derivatives of up to discounted cash flow method is an option-adjusted spread taken 3.3 %. A 10 % change of the surrender assumption for all fixed index from a set of benchmark securities with similar characteristics. A annuities and variable annuities could lead to a change in fair value significant yield increase of the benchmark securities in isolation of the embedded derivatives of up to 3.5 %. could result in a decreased fair value, while a significant yield decrease could result in an increased fair value. However, a 10 % Quantitative description of non-market observable input(s) used for stress of the main non-market observable inputs has only the level 3 portfolios immaterial impact on fair value. Non-market observable Description input(s) Range Equity securities Fixed index annuities Annuitizations 0 % - 25 % For level 2, the fair value is mainly determined using the market Surrenders 0 % - 25 % 1 approach or net asset value techniques for funds. For certain private Mortality n/a equity investments, the funds are priced based on transaction prices Withdrawal benefit election 0 % - 50 % using the cost approach. As there are only few holders of these funds, Variable annuities Surrenders 0.5 % - 35 % 1 the market is not liquid and transactions are only known to Mortality n/a participants. 1_Mortality assumptions are mainly derived from the Annuity 2000 Mortality Table. Level 3 mainly comprise private equity fund investments as well as alternative investments of the Allianz Group, and in most cases are delivered as net asset values by the fund managers. These net asset Financial liabilities for puttable financial values are calculated using material, non-public information about instruments the respective private equity companies. The Allianz Group has only Financial liabilities for puttable financial instruments are generally limited insight into the specific inputs used by the fund managers, required to be recorded at the redemption amount with changes hence a sensitivity analysis is not applicable. The fund’s asset manager recognized in income or equity. The fair value is based on the net asset generally prices the underlying single portfolio companies in line with value or the use of present value techniques. the International Private Equity and Venture Capital Valuation (IPEV) guidelines, using discounted cash flow (income approach) or multiple Significant transfers of financial instruments methods (market approach). For certain investments, the capital carried at fair value invested is considered to be a reasonable proxy for the fair value. In In general, financial assets and liabilities are transferred from level 1 these cases, sensitivity analyses are also not applicable. to level 2 when their liquidity, trade frequency, and activity are no longer indicative of an active market. The same policy applies Financial assets for unit-linked contracts conversely for transfers from level 2 to level 1. For level 2, the fair value is determined using the market or the income Transfers into/out of level 3 may occur due to a reassessment of approach. Valuation techniques applied for the income approach input parameters. mainly include discounted cash flow models as well as the Black- Scholes-Merton model. Financial liabilities for unit-linked contracts are valued based on their corresponding assets. Financial liabilities held for trading This position mainly includes derivative financial instruments. For level 2, the fair value is determined using the income or the market approach. Valuation techniques applied for the income approach mainly include discounted cash flow models as well as the Black-Scholes-Merton model. Main observable input parameters include volatilities, yield curves observable at commonly quoted intervals, and credit spreads observable in the market. For level 3, the fair value is determined using the income or the market approach. Valuation techniques applied for the income approach mainly include discounted cash flow models. A significant proportion of level 3 liabilities represent derivatives embedded in certain life insurance and annuity contracts. Significant non-market observable input parameters include mortality rates and surrender rates. A significant decrease (increase) in surrender rates, in mortality rates, or in the utilization of annuitization benefits could result in a higher (lower) fair value. For products with a high death benefit, surrender rates may show an opposite effect. A significant decrease (increase) in withdrawal benefit election could result in a lower (higher) fair value. A 10 % change of the mortality Annual Report 2021 − Allianz Group 169

Non-financial Statement Page 170 Page 172

Non-financial Statement Page 170 Page 172