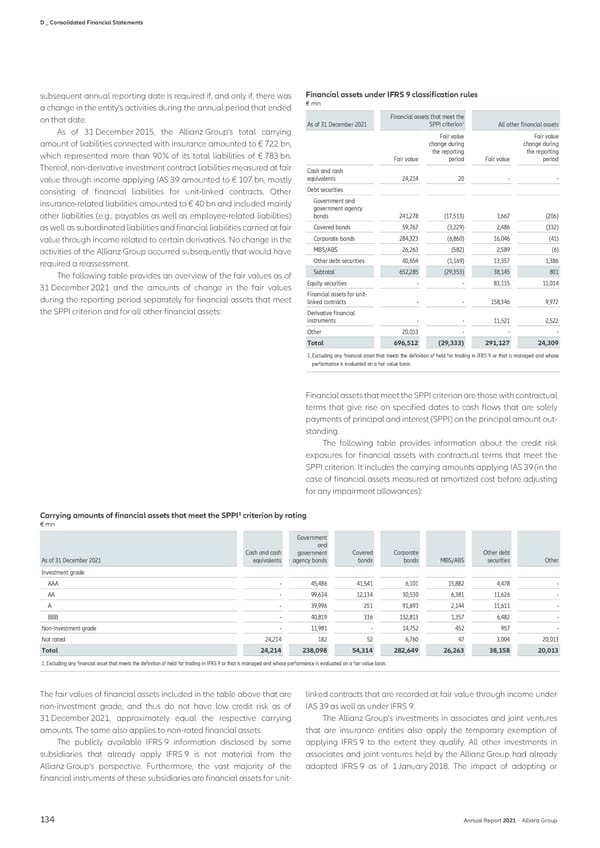

D _ Consolidated Financial Statements subsequent annual reporting date is required if, and only if, there was Financial assets under IFRS 9 classification rules a change in the entity's activities during the annual period that ended € mn on that date. Financial assets that meet the 1 As of 31 December 2021 SPPI criterion All other financial assets As of 31 December 2015, the Allianz Group‘s total carrying Fair value Fair value amount of liabilities connected with insurance amounted to € 722 bn, change during change during which represented more than 90 % of its total liabilities of € 783 bn. the reporting the reporting Fair value period Fair value period Thereof, non-derivative investment contract liabilities measured at fair Cash and cash value through income applying IAS 39 amounted to € 107 bn, mostly equivalents 24,214 20 - - consisting of financial liabilities for unit-linked contracts. Other Debt securities insurance-related liabilities amounted to € 40 bn and included mainly Government and government agency other liabilities (e.g., payables as well as employee-related liabilities) bonds 241,278 (17,513) 3,667 (206) as well as subordinated liabilities and financial liabilities carried at fair Covered bonds 59,767 (3,229) 2,486 (332) value through income related to certain derivatives. No change in the Corporate bonds 284,323 (6,860) 16,046 (41) activities of the Allianz Group occurred subsequently that would have MBS/ABS 26,263 (582) 2,589 (6) required a reassessment. Other debt securities 40,654 (1,169) 13,357 1,386 The following table provides an overview of the fair values as of Subtotal 652,285 (29,353) 38,145 801 31 December 2021 and the amounts of change in the fair values Equity securities - - 83,115 11,014 during the reporting period separately for financial assets that meet Financial assets for unit- linked contracts - - 158,346 9,972 the SPPI criterion and for all other financial assets: Derivative financial instruments - - 11,521 2,522 Other 20,013 - - - Total 696,512 (29,333) 291,127 24,309 1_Excluding any financial asset that meets the definition of held for trading in IFRS 9 or that is managed and whose performance is evaluated on a fair value basis. Financial assets that meet the SPPI criterion are those with contractual terms that give rise on specified dates to cash flows that are solely payments of principal and interest (SPPI) on the principal amount out- standing. The following table provides information about the credit risk exposures for financial assets with contractual terms that meet the SPPI criterion. It includes the carrying amounts applying IAS 39 (in the case of financial assets measured at amortized cost before adjusting for any impairment allowances): 1 Carrying amounts of financial assets that meet the SPPI criterion by rating € mn Government and Cash and cash government Covered Corporate Other debt As of 31 December 2021 equivalents agency bonds bonds bonds MBS/ABS securities Other Investment grade AAA - 45,486 41,541 6,101 15,882 4,478 - AA - 99,634 12,134 30,530 6,381 11,626 - A - 39,996 251 91,693 2,144 11,611 - BBB - 40,819 336 132,813 1,357 6,482 - Non-investment grade - 11,981 - 14,752 452 957 - Not rated 24,214 182 52 6,760 47 3,004 20,013 Total 24,214 238,098 54,314 282,649 26,263 38,158 20,013 1_Excluding any financial asset that meets the definition of held for trading in IFRS 9 or that is managed and whose performance is evaluated on a fair value basis. The fair values of financial assets included in the table above that are linked contracts that are recorded at fair value through income under non-investment grade, and thus do not have low credit risk as of IAS 39 as well as under IFRS 9. 31 December 2021, approximately equal the respective carrying The Allianz Group’s investments in associates and joint ventures amounts. The same also applies to non-rated financial assets. that are insurance entities also apply the temporary exemption of The publicly available IFRS 9 information disclosed by some applying IFRS 9 to the extent they qualify. All other investments in subsidiaries that already apply IFRS 9 is not material from the associates and joint ventures held by the Allianz Group had already Allianz Group’s perspective. Furthermore, the vast majority of the adopted IFRS 9 as of 1 January 2018. The impact of adopting or financial instruments of these subsidiaries are financial assets for unit- 134 Annual Report 2021 − Allianz Group

Non-financial Statement Page 135 Page 137

Non-financial Statement Page 135 Page 137